Filed under: Earnings, Retail, Market News

Family Dollar (FDO) says its quarterly earnings rose by less than three percent, falling shy of Wall Street expectations.

But the company had plenty of excuses for the shortfall: It blames the economy, the weather, and the delay in tax refunds earlier this year.

And Family Dollar doesn’t see things getting a whole lot better. It revised its earnings forecast for 2013 significantly lower for the second time this year.

But not everything is bleak. Sales rose by 18 percent in the latest quarter, meeting expectations, as the company continued to add stores at a rapid pace. It opened 500 new locations last year and is expected to add that many again this year. It now has more than 7,000 stores. And the sale trend improved in February as customers began to receive their tax refund checks.

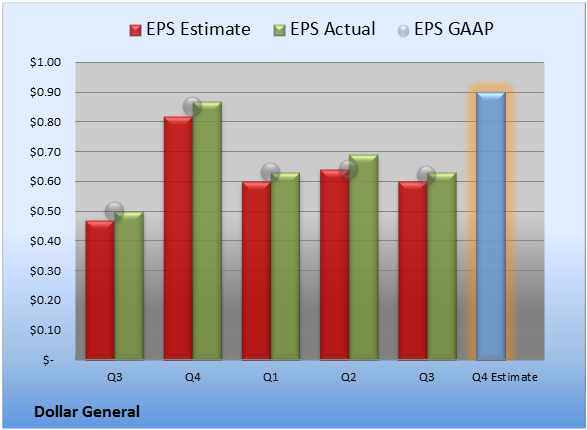

But analysts say there are bigger trends working against Family Dollar and its main rivals – Dollar General (DG) and Dollar Tree (DLTR). The biggest factor is that Walmart (WMT) has stepped up its competition to win the dollars of hard-pressed shoppers by lowering prices.

Family Dollar is trying to make itself a one-stop destination by adding cigarettes, Pepsi (PEP) products, gift cards and magazines. This strategy may draw more customers into its stores, but these are generally very low margin products compared to apparel and other items – and that has pressured profitability.

That’s in contrast to what happened in recent years, during and right after the recession. Sales and earnings soared as low-income shoppers flocked to dollar stores.

Family Dollar has also underperformed on Wall Street. So far this year, its stock is down seven percent. By comparison, both Dollar General and Dollar Tree have gained 15 percent this year.

It was just over a year ago that Family Dollar rejected a $7 billion buyout offer from Trian Group, the firm run by activist investor Nelson Peltz.

-Produced by Drew Trachtenberg

%Gallery-181478%

Permalink | Email this | Linking Blogs | Comments

Source: FULL ARTICLE at DailyFinance