By Seth Jayson, The Motley Fool

Filed under: Investing

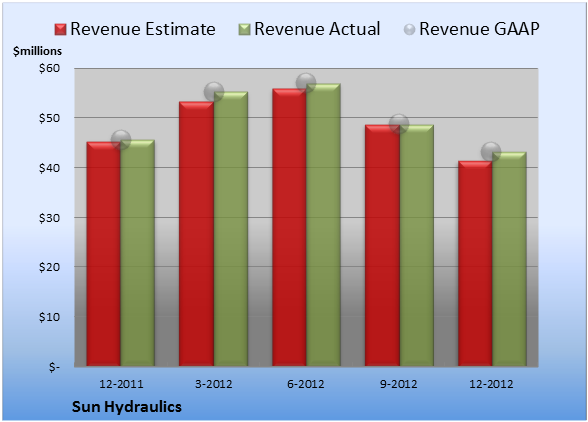

Sun Hydraulics (NAS: SNHY) reported earnings on March 4. Here are the numbers you need to know.

The 10-second takeaway

For the quarter ended Dec. 29 (Q4), Sun Hydraulics beat expectations on revenues and beat expectations on earnings per share.

Compared to the prior-year quarter, revenue dropped. GAAP earnings per share grew.

Gross margins grew, operating margins shrank, net margins expanded.

Revenue details

Sun Hydraulics reported revenue of $43.2 million. The three analysts polled by S&P Capital IQ expected sales of $41.4 million on the same basis. GAAP reported sales were 5.3% lower than the prior-year quarter’s $45.7 million.

Source: S&P Capital IQ. Quarterly periods. Dollar amounts in millions. Non-GAAP figures may vary to maintain comparability with estimates.

EPS details

EPS came in at $0.26. The three earnings estimates compiled by S&P Capital IQ averaged $0.23 per share. GAAP EPS of $0.26 for Q4 were 8.3% higher than the prior-year quarter’s $0.24 per share.

Source: S&P Capital IQ. Quarterly periods. Non-GAAP figures may vary to maintain comparability with estimates.

Margin details

For the quarter, gross margin was 37.0%, 10 basis points better than the prior-year quarter. Operating margin was 21.9%, 100 basis points worse than the prior-year quarter. Net margin was 15.5%, 220 basis points better than the prior-year quarter.

Looking ahead

Next quarter’s average estimate for revenue is $50.2 million. On the bottom line, the average EPS estimate is $0.34.

Next year’s average estimate for revenue is $204.0 million. The average EPS estimate is $1.40.

Investor sentiment

The stock has a five-star rating (out of five) at Motley Fool CAPS, with 1,308 members out of 1,325 rating the stock outperform, and 17 members rating it underperform. Among 406 CAPS All-Star picks (recommendations by the highest-ranked CAPS members), 404 give Sun Hydraulics a green thumbs-up, and two give it a red thumbs-down.

Of Wall Street recommendations tracked by S&P Capital IQ, the average opinion on Sun Hydraulics is hold, with an average price target of $28.50.

Looking for alternatives to Sun Hydraulics? It takes more than great companies to build a fortune for the future. Learn the basic financial habits of millionaires next door and get focused stock ideas in our free report, “3 Stocks That Will Help You Retire Rich.” Click here for instant access to this free report.

- Add Sun Hydraulics to My Watchlist.

The article Sun Hydraulics Beats on Both Top and Bottom Lines originally appeared on Fool.com.

Seth Jayson had no position in any company mentioned here at …read more

Source: FULL ARTICLE at DailyFinance