By Sean Williams, The Motley Fool

Filed under: Investing

Although we don’t believe in timing the market or panicking over market movements, we do like to keep an eye on big changes — just in case they’re material to our investing thesis.

What: Shares of Krispy Kreme Doughnuts , donut maker extraordinaire, shed as much as 10% after reporting its fourth-quarter earnings results. However, shares have retraced much of their losses and are down less than 4% as of this writing.

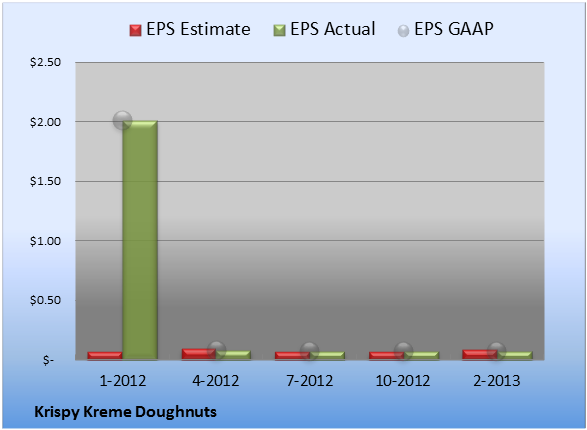

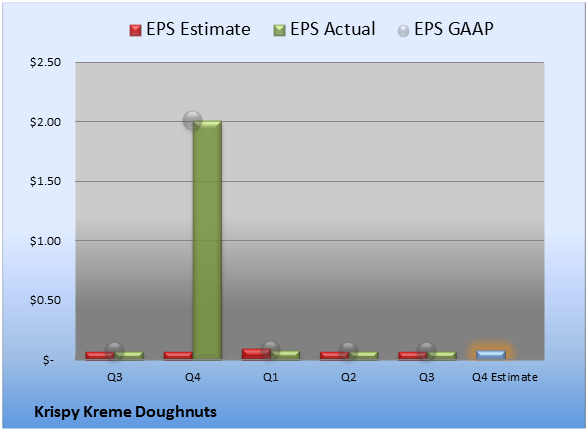

So what: For the quarter, Krispy Kreme reported a robust 16% increase in revenue, to $118.1 million over the year-ago period, as adjusted net income soared 85%, to $0.11 per share. Wall Street had also been expecting $0.11 in EPS, but was looking for only $116.5 million in revenue. Most importantly, same-store sales growth of 7.5% shows continued emphasis on driving traffic and higher ticket sales. Looking ahead, Krispy Kreme forecast full-year 2014 EPS of $0.53-$0.57, which is noticeably higher than the $0.52 the Street expected, but not nearly high enough for investors who had bet on a fatter figure.

Now what: All told, this was an exceptionally good report from Krispy Kreme, and it probably didn’t deserve the 10% lashing it took earlier in the session. I’m not a huge fan of the run its share price has had, and feel that investors may have become a bit exuberant with its outlook; however, Krispy Kreme‘s management continues to rely on menu innovation, signature coffee blends, and expansion into emerging markets as its keys to growing the business. From a bystander’s viewpoint, this was a solid quarter.

Craving more input? Start by adding Krispy Kreme Doughnuts to your free and personalized Watchlist so you can keep up on the latest news with the company.

Profiting from our increasingly global economy can be as easy as investing in your own backyard. The Motley Fool’s free report, “3 American Companies Set to Dominate the World” shows you how. Click here to get your free copy before it’s gone.

The article Why Krispy Kreme Doughnuts Shares Were Glazed, Temporarily originally appeared on Fool.com.

Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.

Try any of our Foolish newsletter services free for 30 days. We Fools don’t all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.

(function(c,a){window.mixpanel=a;var b,d,h,e;b=c.createElement(“script”);

…read more

Source: FULL ARTICLE at DailyFinance