By Michael Lewis, The Motley Fool

Filed under: Investing

Office ergonomics are something we think little about but are greatly affected by, if subconsciously. Office furniture design house Herman Miler is one of the best in the business, combining amazing functionality with style and comfort. Items as simple as desk chairs (we know how important this can be) can sell for more than $1,000, and full office systems many times that. The company’s price point and production methods have helped create better-than-expected gross margins, most recently yielding a 23% increase in adjusted earnings per share. At 15 times forward earnings, and with strong prospects ahead, this furniture design company is trading at a discount to peers and may be the best-in-class. Here’s what you need to know about Herman Miller.

Comfortable earnings

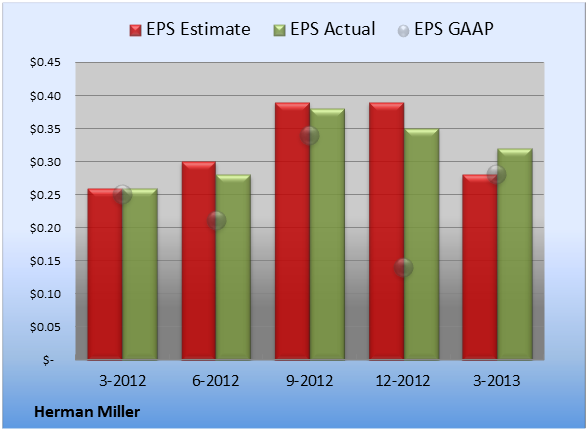

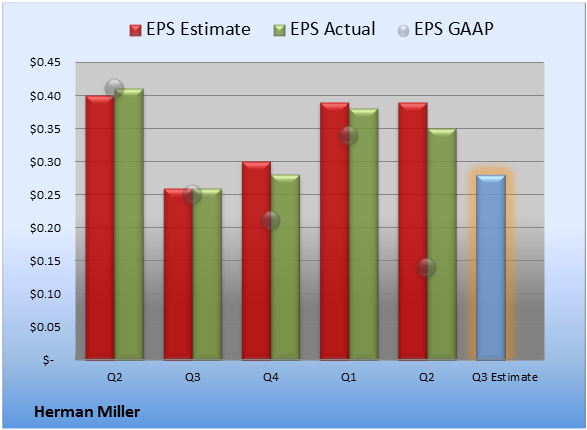

The most recent quarter marks a turnaround point for Herman Miller. In the four quarters preceding, the company had year-over-year declines in sales figures. For the past couple of years, the North American market has been particularly hard for the company because of soft government demand. However, the company has recently seen a 5% uptick in sales along with a 10-point pickup in orders for the region — certainly encouraging, and going along with analyst expectations for the industry.

Outside North America, things look much better. Sales during the third quarter grew by an impressive 17%, and future orders were up 3% from the prior year. As is typical of many high-priced design businesses, high-margin items selling well in Asia were largely responsible for the growth.

The company’s seating line is its classic offering — attractive sitting solutions (yes, that’s a term) that are incredibly comfortable and made for some serious, long-term sitting. The current product cycle appears to be at its end, with a major overhaul coming this spring. As the cycle renews, this should help boost sales in subsequent quarters.

As far as numbers go, the company beat the Street on the bottom line but missed on revenues. Sales came in at a 6% premium to the prior year’s quarter, with $424 million. The majority of the company’s sales comes from North America. In the third quarter, the region was responsible for $285 million, and non-North American sales were at $91 million. The company’s Specialty and Consumer segment continues to outperform, up 13% to $47 million. The aforementioned gross margin, at 34.2% (excluding legacy pension expenses), was higher than the company expected and drove bottom-line earnings to their double-digit gains.

Herman Miller made $30 million in free cash flow for the quarter.

Looking forward, the company expects another $430 million to $450 million in sales to cap off the year, representing a 2% to 7% increase over the prior year’s numbers. Gross margins are expected to remain at their elevated level, and EPS are targeted to come in at $0.34 to $0.38, adjusted.

What it all means

So Herman Miller is clearly navigating the tepid economic recovery in the United States quite well, with the exception of its …read more

Source: FULL ARTICLE at DailyFinance