By Seth Jayson, The Motley Fool

Filed under: Investing

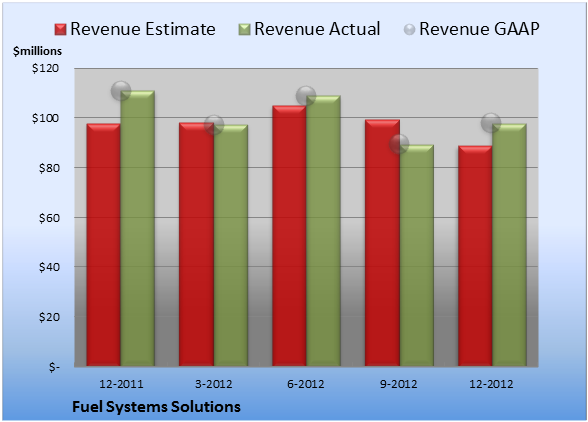

Fuel Systems Solutions (NAS: FSYS) reported earnings on March 8. Here are the numbers you need to know.

The 10-second takeaway

For the quarter ended Dec. 31 (Q4), Fuel Systems Solutions beat expectations on revenues and beat expectations on earnings per share.

Compared to the prior-year quarter, revenue shrank. Non-GAAP earnings per share dropped significantly. GAAP earnings per share shrank to a loss.

Gross margins were steady, operating margins dropped, net margins dropped.

Revenue details

Fuel Systems Solutions chalked up revenue of $98.0 million. The eight analysts polled by S&P Capital IQ looked for net sales of $88.8 million on the same basis. GAAP reported sales were 12% lower than the prior-year quarter’s $111.0 million.

Source: S&P Capital IQ. Quarterly periods. Dollar amounts in millions. Non-GAAP figures may vary to maintain comparability with estimates.

EPS details

EPS came in at $0.01. The eight earnings estimates compiled by S&P Capital IQ averaged -$0.03 per share. Non-GAAP EPS of $0.01 for Q4 were 86% lower than the prior-year quarter’s $0.07 per share. GAAP EPS were -$1.05 for Q4 against $0.07 per share for the prior-year quarter.

Source: S&P Capital IQ. Quarterly periods. Non-GAAP figures may vary to maintain comparability with estimates.

Margin details

For the quarter, gross margin was 21.8%, much about the same as the prior-year quarter. Operating margin was 1.3%, 40 basis points worse than the prior-year quarter. Net margin was -21.4%, much worse than the prior-year quarter. (Margins calculated in GAAP terms.)

Looking ahead

Next quarter’s average estimate for revenue is $93.9 million. On the bottom line, the average EPS estimate is $0.10.

Next year’s average estimate for revenue is $414.1 million. The average EPS estimate is $0.58.

Investor sentiment

The stock has a four-star rating (out of five) at Motley Fool CAPS, with 471 members out of 531 rating the stock outperform, and 60 members rating it underperform. Among 104 CAPS All-Star picks (recommendations by the highest-ranked CAPS members), 81 give Fuel Systems Solutions a green thumbs-up, and 23 give it a red thumbs-down.

Of Wall Street recommendations tracked by S&P Capital IQ, the average opinion on Fuel Systems Solutions is hold, with an average price target of $19.83.

The rich are different than you and me: They might not notice the moneymaking stories right under our noses. In our new report, “Middle-Class Millionaire-Makers: 3 Stocks Wall Street’s Too Rich to Notice,” we give you three Peter Lynch-inspired buy-what-you-know stocks for the 99%. Click here for instant access to this free report.

- Add Fuel Systems Solutions to My Watchlist.

The …read more

Source: FULL ARTICLE at DailyFinance