By Rich Duprey, The Motley Fool

Filed under: Investing

All good things must come to an end. After seven straight days of gains, the S&P 500 finally lost four points. The Dow Jones Industrial Average, however, continued its string of up days, tacking on another three points to make it eight consecutive days of new highs.

As the Fool’s Jeremy Bowman pointed out the other day, a better economic outlook here at home is driving the market‘s euphoria while much of the rest of the world teeters on collapse. So don’t go running over the cliff with them like a bunch of lemmings: This could just be a temporary situation. Let’s first see whether they had good reason to fall, as panic-fueled routs can sometimes lead to excellent buying opportunities.

|

Company |

% Change |

|---|---|

|

Diamond Foods |

(9.7%) |

|

Perfect World |

(8.8%) |

|

Yandex |

(8%) |

That’s nuts

Last week nut grower Diamond Foods surged higher on no apparent news, which I suggested would end up being a short-term phenomenon because there was no fundamental basis for the rise. That was borne out by yesterday’s crash after Diamond reported earnings that were only in line with analyst expectations.

Despite having lost the Pringles brand to Kellogg following its accounting shenanigans debacle that led to a restatement of its financials, it’s still apparent Diamond Foods wants to be a snack-food player. Starting with its second-quarter results, it’s reporting in two segments now: nuts and snacks. The latter saw revenues rise 7% to $105 million, while nut revenues plummeted almost 30% as volumes cratered 37% from the year-ago period.

Yet it could have been so much more. Kellogg reported fourth-quarter earnings last month showing net sales soaring 18%, as Pringles drove most of the gains. As I noted at the time, “Without the acquisition, sales growth still would have come in at 5.3%, its biggest gain in more than a year, but it shows what Diamond could have enjoyed had it won the brand.” The stock is down almost 12% now from its recent highs.

Game over?

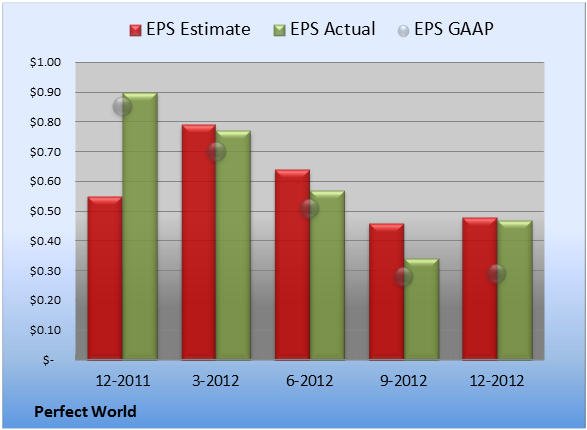

Chinese Web games operator Perfect World also reported earnings the other day in line with expectations, but its outlook for the future is what sank the stock yesterday. It projected first-quarter sales to come in between 592 million yuan, or about $95 million at current exchange rates, to 619 million yuan, which is well below the 643 million yuan consensus estimate of analysts.

Management contends, though, that it’s investing in the future of its business, so that while it makes current-period results weaker than anticipated, it will pay off later on. Perfect World decelerated its in-game promotional activities and focused instead on its pipeline as well as content enhancements for its existing titles, but the market apparently didn’t buy into that argument.

I’ve noted on numerous occasions I’m not a fan of the free-to-play/pay-to-play-more online gaming business model, and I believe the moves by …read more

Source: FULL ARTICLE at DailyFinance