By Rich Duprey, The Motley Fool

Filed under: Investing

The old investing maxim “sell in May and go away” means we’re quickly approaching the time when the incredible run of the Dow Jones Industrial Average over the past three months will be coming to a close. Yesterday’s five-point loss could be the signal that the market is topping here, and with Europe doing all it can to stop the spread of a financial contagion after its bailout of Cyprus, there seems little reason to believe this bull market will continue much longer.

Yesterday’s big loser was Hewlett-Packard, the first quarter’s big winner, though after a 68% gain over the past three months, a small 2% loss is no big deal. But the landscape for computers hasn’t changed, so now comes the point where the turnaround has to gain traction on its own. I’m not so certain it will, though a broad overview of the markets suggests there are still worse places to be standing right now.

Canary in the coal mine

Coal miner Walter Energy took it on the chin (again) yesterday, falling 8% as the ISM manufacturing index posted its biggest miss to expectations in a year, coming in at 51.3 compared with forecasts of 54.0. The bigger worry, however, is new orders falling all the way down to 51.4 from 57.8, which, coupled with a pullback in China‘s economy, diminishes the prospects for renewed industrial demand and, in turn, greater coal demand. Arch Coal, Peabody Energy , and Consol Energy all tumbled 3% or more yesterday.

Analysts see a particularly tough year ahead for Walter because of the weak pricing environment. It has significant cash obligations coming due this year, with Wall Street looking askance at the $150 million or so in interest payments and total cash obligations of $365 million, both of which combine to put it between a financial rock and a hard place.

It faces outside pressure as well from shareholders agitating for change. Hedge-fund operator SAC Capital Partners recently reported a new 5% stake in the miner, while Audley Capital has publicly expressed doubts about management’s capabilities to turn the company around and wants to oust some directors in favor of its own five-man slate.

As coal miners remain under the gun, there appear to be few catalysts in front of Walter to change its downward trajectory.

Wearing the dunce cap

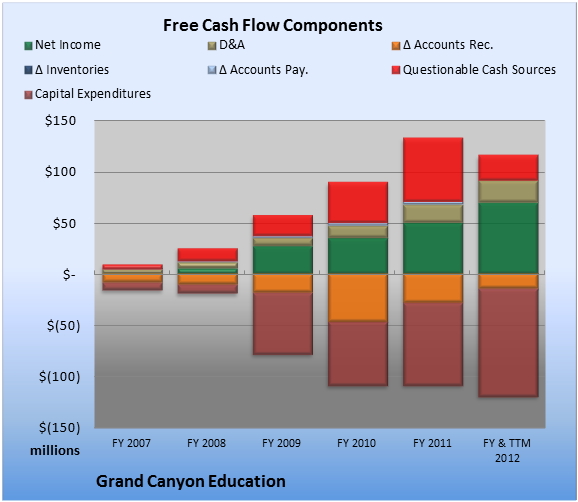

For-profit educators got schooled yesterday as well, with ITT Educational Services falling almost 9%, Grand Canyon Education dropping 5%, and Corinthian Colleges and Career Education both falling about 3% on the day. The one bright spot was Apollo Group , which rose about 1.5% and is up more than 3% since reporting better-than-expected earnings last week.

Yet even in beating Wall Street forecasts, Apollo showed what the problems are facing the sector: falling revenues, higher expenses, and dwindling student enrollments. When ITT reported fourth-quarter earnings in January, it saw all of those same factors, but it didn’t have the luxury of beating expectations. First-quarter results …read more

Source: FULL ARTICLE at DailyFinance